How can you leverage tax loss harvesting?

Reduce your tax bill now

There are a few weeks left to take advantage of tax loss harvesting as a tax management tool for the current tax year. First, log into your brokerage account and scan the “total gain or loss” column for “red” (aka negative) numbers. If you have a loss, this might be the time to sell that asset and realize the loss. Why? Keep reading.

For many years, I was of the mindset that gains or losses weren’t “real” unless I sold the investment (realizing the gain or loss), and why on earth would I ever sell the investment at a loss? Wouldn’t it be better to just wait for its price to rebound? I also thought tax loss harvesting was a joke, and that applying my losses to reduce up to $3,000 in income would make little or no difference to me financially, and seemed like a lot of hassle and audit risk. What I did not understand then was that losses can also be applied to capital gains from other stock sales in an unlimited fashion, and can be carried over year after year until they are used. Thus, selling at a loss might reduce your tax liabilities for years to come, giving you more money to invest now for greater returns over the long timeframe.

In a nutshell and oversimplified, tax loss harvesting is when an investor sells a stock, mutual fund, exchange traded fund (ETF) or other investment at a loss in order to apply that loss to counteract the tax impact of other capital gains (in addition to reducing income a tiny bit, currently limited to $3,000).

When would I use this? Let’s say you invested in a company that was purchased by another company, and the sale was at a stock price substantially higher than what you paid for the stock. You have no choice but to sell the stock because the company does not exist in its current iteration anymore, and that taxable gain (the difference between what you paid for the stock, i.e. the basis, and what it is now being purchased for) is now a ticking tax bill time bomb, especially if you are in a higher tax bracket. But if you could sell some other investments at a loss, that loss could be applied to the gain to reduce and potentially eliminate it. The aggregate of gains and losses can reduce your overall tax liability by reducing the amount of gains that you have to pay taxes on. In addition to reducing your current year tax bill, you can also use the investment sales to rebalance your portfolio to align with your asset allocation (such as when a good or bad year took you more than 5% away from your target percentages).

For those with a bit more risk tolerance, you can also sell a security or investment to take the loss and apply it to gains now and in the future, and then repurchase the investment after 30 days (excluding the day of sale) have passed. That way, you still benefit from any long-term value upswing, but have harvested losses to use now to reduce your tax liability (kind of like when Wimpy tells Popeye, "I'll gladly pay you Tuesday for a hamburger today.”) It is important to understand that, when you plan to repurchase a similar or same investment, what you are really doing is deferring taxes, not eliminating them. This is because the repurchase may “reset” your basis at a lower purchase price, creating the potential for a larger taxable gain at the ultimate disposition of the asset.

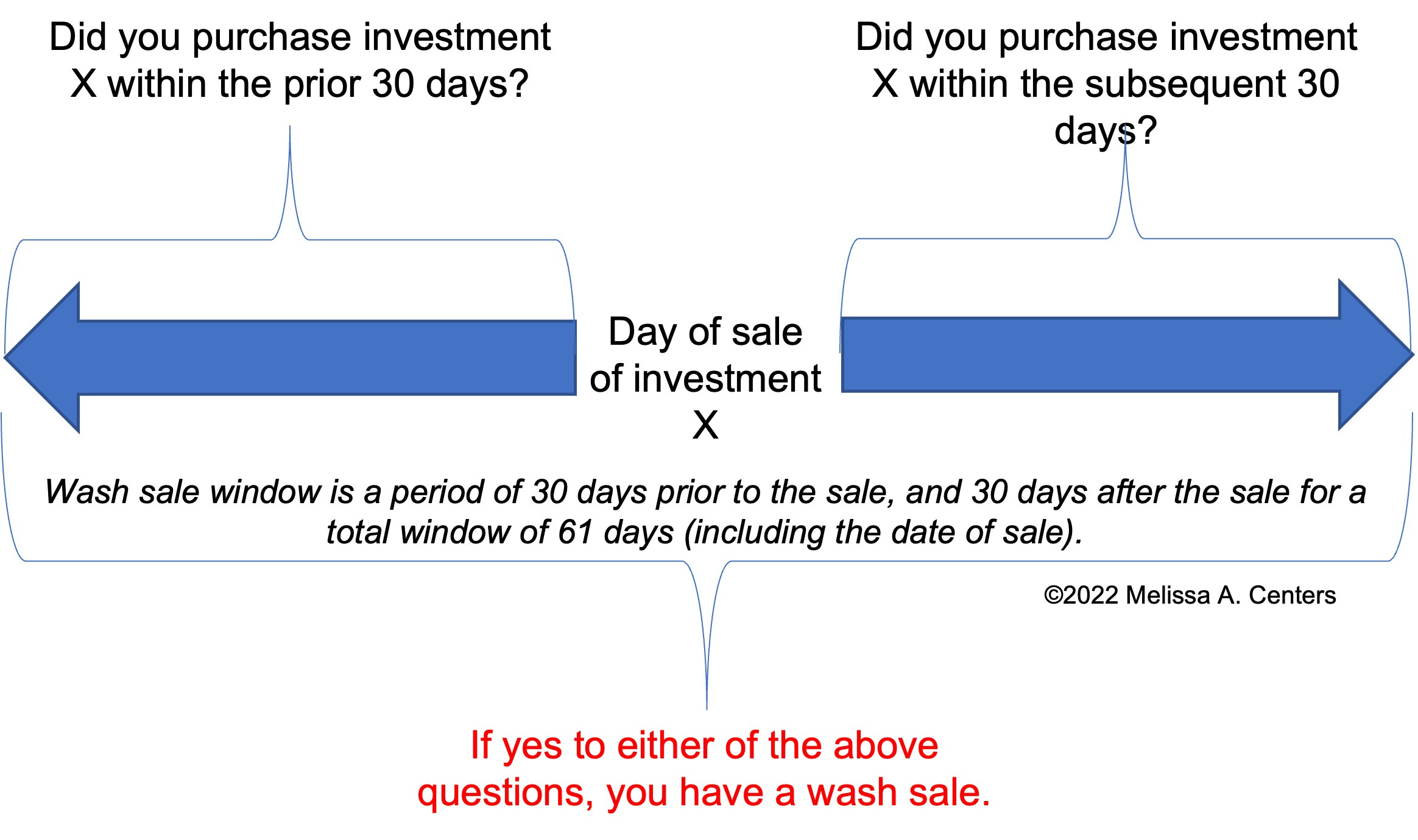

Why 30 days? When you are selling an investment that still exists (meaning the company has not been bought and the stock redeemed), like an individual stock, a mutual fund or an ETF, you also have to be careful of wash sales. In order for the losses associated with the sale of an investment to be applied to current income and other capital gains, it cannot be a wash sale, meaning that the investor cannot buy a substantially identical investment in the period that includes 30 days prior and 30 days after the sale. Wash sales are not illegal, but they eliminate your ability to apply certain losses to offset gains, rendering your actions useless in any attempt to reduce your tax liability.

When considering tax loss harvesting for individual stocks, the substantially identical investment is an easy test…you cannot have already bought the same individual stock for the 30 days prior to the sale, or purchase the stock again within 30 days after your tax loss sale. For example, you will have a wash sale if you buy 100 shares of Amazon stock on October 1 for $1000/share, then sell part or all of your holdings on October 25 for $900/share. Conversely, if you bought 100 shares of Amazon stock on September 1 for $1000/share, then sold it on November 3 for $900/share, you don’t have a wash sale unless you then “rebuy” Amazon stock during the period of 30 days after November 3 (not including November 3). In these examples, even though you have a loss, that loss (or at least a portion of it) is considered a wash sale and cannot be used to reduce other gains.

For mutual funds and ETFs, there is not a lot of formal guidance from the IRS related to “substantially identical” and advisors tend to be all over the place on what is allowed. I take the conservative approach (shocking, I realize) and assume “substantially identical” will include a number of things, like funds with similar investment objectives, funds that share a single fund manager, or funds tied to the same index. I use fund compare tools (such as those available on Vanguard) to compare investments to see how similar they are, and I save my findings in the event I ever need to prove why they weren’t substantially identical in an audit setting (you could potentially use facts about the two funds like materially different top holdings, turnover rates, expense ratios, and the like to prove they were not substantially identical). Also, contrary to the opinions of some, I do not think simply switching from an ETF to a “sister” mutual fund or vice versa (for example, Vanguard’s popular S&P 500 ETF, VOO, is also available as a mutual fund, VFIAX and VFFSX) is enough to exclude your new investment from wash sale rules because I would argue these two vehicles are substantially identical.

Some other “gotchas” to consider when doing tax loss harvesting is whether you own the same or substantially similar investment in other accounts, or whether your spouse owns the same investment vehicle. Why? Wash sales apply between different accounts (including at different brokerage houses) and between spouses (and potentially children at home). To make this process more difficult, even reinvested distributions in any account in your household (where you automatically use distributions like dividends or capital gains within a fund to “purchase” more of the particular investment) can trigger a portion of the loss as a “wash sale” because of the purchase involved in the reinvestment.

So, how was that for complicated?

Click here to return to Money, Money, Money - Retirement and Investment Checklist.